The Greenfield Gambit

How Jingzhou Is Engineering Itself Into China’s Paper Capital

The city with no heritage has one advantage the heritage city will never recover: it can rebuild from zero while the old capital is still arguing about its first retrofit.

Every industrial cluster eventually freezes.

The mills age. The land fills. The environmental permits become locked. The technology stack becomes a debt, not an asset. The capital that made the city rich becomes the capital that cannot afford to stop production long enough to modernize.

The old capital is not a fortress. It is a trap. It cannot leapfrog. It can only patch.

This is the opening.

A city with no paper heritage; no century old mills, no family dynasties, no generational craft knowledge, faces no such trap. It has nothing to retrofit. Nothing to phase in while keeping production alive. Nothing to negotiate with unions or environmental regulators who remember the last shutdown.

It can build from greenfield. Install the technology that the old capital admired at trade shows but could not afford to install. Recruit the anchors that the old capital lost because it had no space. Declare itself the new capital before a single mill is operational; not as marketing, but as a policy weapon that pre-empts any competitor from claiming the same title.

This is not a story about paper.

It is a story about what happens when a replaceable city realizes that having no past is not a weakness. It is the only way to win against a frozen incumbent.

Jingzhou understood this.

And the old paper capitals are still standing on their saturated ground, watching.

The Replaceable Pass through

What Jingzhou was before the pivot.

In 1995, Jingzhou’s GDP was 19.05 billion yuan. Its per capita GDP was 4,150 yuan.1

The city occupied 14,104 square kilometers of the Jianghan Plain; the most fertile alluvial land in Hubei and sat at the confluence of the Yangtze and Han rivers, two of China’s most consequential waterways.2

By geography alone, Jingzhou should have been rich.

It was not.

The same year, Hubei’s per capita GDP averaged 3,671 yuan; already below the national average of 5,091 yuan.3 But Jingzhou trailed even that modest baseline. Wuhan, 200 kilometers upstream, recorded 8,609 yuan per capita more than double Jingzhou’s figure. Yichang, 120 kilometers to the west, recorded 4,728 yuan.4

Jingzhou was not just poorer than the provincial capital. It was poorer than the provincial average. And its economic structure revealed why.

The Trap

Of Jingzhou’s 19.05 billion yuan GDP in 1995, the primary sector (agriculture) contributed 9.67 billion yuan; over 50 percent.5

This was not an economy. It was an extraction zone.

The city produced grain, cotton, oilseeds and aquatic products. It shipped them upriver to Wuhan for processing or downriver to Shanghai for export. The value left. What remained was subsistence: a rural population with no industrial employment, no processing infrastructure and no claim on the margin their labor generated.

Jingzhou was not a node. It was a pass through.

The city’s position on the map was its curse. Between Wuhan (the political and industrial core of central China) and Yichang (the energy fortress anchored by the Three Gorges Dam), Jingzhou occupied the flat space that neither wanted to develop and neither could afford to lose. Wuhan needed Jingzhou’s grain. Yichang needed Jingzhou’s flat land for resettlement and logistics. But neither needed Jingzhou to process anything.

The region was structurally redundant. If Jingzhou disappeared, the grain would still travel. The Yangtze would still flow. The system would reroute through Qianjiang or Xiantao; smaller, flatter, equally replaceable.

Jingzhou was not underdeveloped. It was structurally trapped, condemned to produce raw value and ship it elsewhere.

The Binding Constraint

The constraint was not land. The Jianghan Plain is absurdly fertile, capable of producing three crops per year on well drained fields.

The constraint was not labor. Jingzhou’s population in 1995 exceeded 4.5 million, a workforce large enough to staff any factory.

The constraint was not water. The Yangtze and Han rivers provided more fresh water than any industrial park could consume.

The constraint was permission.

Jingzhou had no authorization to industrialize. The national development strategy of the 1980s and 1990s prioritized coastal provinces; Guangdong, Fujian, Zhejiang, Jiangsu where foreign capital could enter through Hong Kong and Shanghai. Inland provinces were assigned the role of commodity suppliers: grain from the plains, coal from Shanxi, oil from Daqing.

Jingzhou was not failing. It was performing exactly the function assigned to it.

And that function was replaceable.

Permission and Passage

The moment the trajectory bent.

In 1995, Jingzhou was a replaceable pass through: 51 percent of its GDP from agriculture, zero paper mills, zero national policy designation, zero claim on the value it generated.

By 2025, the city had recruited four publicly listed paper giants, secured 55+ billion RMB in committed investment and formally declared itself Central China’s Packaging Paper Capital. Key products include premium paper goods... with leading enterprises such as Nine Dragons, Shanying, Longchen, Xianhe, Paima.6

The transformation required two things Jingzhou did not possess in 1995: permission to industrialize and passage to move output.

Both arrived between 2011 and 2021. The sequence matters. Permission came first. Then passage. Then the anchors.

The First Catalyst: National Zone Status (2011)

Jingzhou Economic and Technological Development Zone was founded in 1992 as a provincial level zone, one of dozens across Hubei with no special standing.7 For nearly two decades, it remained exactly that: provincial, peripheral, underfunded.

In June 2011, the State Council upgraded the zone to national level economic and technological development zone status.8

This was not a ceremonial rename. National status unlocked three things:

Direct access to central government infrastructure funds, bypassing provincial allocation

Preferential land conversion quotas, allowing agricultural land to be rezoned for industrial use

Elevated investment approval authority, meaning larger projects could be cleared without Beijing level review

The zone’s footprint expanded from a modest industrial park to 209 square kilometers (and later to 318.5 square kilometers), with a population of 180,000 and over 1,000 industrial enterprises.9

In December 2011, the National Development and Reform Commission designated Jingzhou a National Industrial Transfer Demonstration Zone, one of only a handful nationwide. The designation was explicit: Jingzhou was authorized to receive industries relocating from the crowded, environmentally constrained coastal provinces.

The provincial government moved immediately. The 2012 Hubei Provincial Government Work Report announced the “Overall Plan for the Acceleration of Jingzhou’s Revitalization,” naming machinery, textile, auto parts, agro-processing, and sylvite chemistry as pillar industries.10 The plan was not aspirational. It was a binding document with allocated budget lines.

The binding constraint removed first was policy permission. Jingzhou had water, land and labor in 1995. It lacked the legal authorization to convert those assets into industrial capacity. National zone status in 2011 supplied that authorization.

The Second Catalyst: Regional Center City Designation (2021)

National zone status gave Jingzhou permission to industrialize. But it did not give Jingzhou priority.

Between 2011 and 2021, the city remained one of several medium sized industrial bases in Hubei behind Wuhan, behind Xiangyang, behind Yichang. It could attract factories, but it could not demand that the provincial government orient logistics, rail and energy infrastructure around its growth.

The second catalyst arrived in 2021.

The *Hubei Province 14th Five-Year Plan for New Urbanization (2021–2035)* formally designated Jingzhou as a regional中心城市 (regional central city) one of only six comprehensive regional centers in the province, alongside Huangshi, Shiyan, Jingmen, Xiaogan and Huanggang.11

The designation carried specific language: “Support Jingzhou in building a central city in the Two Lakes Plain (Dongting and Jianghan) of the middle Yangtze, creating demonstration zones for green innovation, rural revitalization, industrial transfer, cultural heritage and modern comprehensive transportation.”12

Hubei Party Secretary Ying Yong, during a 2021 inspection of Jingzhou, added: “Jingzhou is the root of Chu culture. Hubei is the center of central China; Jingzhou is the center of Hubei. It occupies a special and important position in the province’s development landscape. Central Hubei needs a central city. Jingzhou is duty bound.”13

The 2021–2035 Urbanization Plan further specified that Jingzhou would be elevated to a Type II Large City (population 1–3 million in the urban core) by 2035, placing it in the same tier as Huangshi, Shiyan and Xiaogan.14

The second constraint removed was infrastructure priority. Regional center status obligated the provincial and national governments to route transportation, logistics, and energy projects through Jingzhou rather than around it.

The Enabling Infrastructure: The Bridge That Changed the Map

Policy permission and regional priority would have meant little without physical access.

Jingzhou’s curse had always been its position between Wuhan and Yichang, close enough to be overshadowed, far enough to be bypassed. The Yangtze was a barrier as much as a resource. South of the river,公安 and Shishou counties remained agricultural backwaters with no rail connection to the northern industrial core.

The Jingzhou Yangtze River Rail-cum-Road Bridge (also known as the Gong’an Bridge) changed this.15

Construction began in December 2012. The bridge spans 6,317 meters, with a main span of 518 meters, carrying a double track heavy rail line on its lower deck and a four lane highway above. Total investment: 1.8 billion RMB.

The bridge opened in two stages:

August 2019: Highway deck opened to traffic

September 2019: Rail deck opened, integrated into the Haolebaoji-Ji’an Railway (HaO-Ji Railway) China’s North to South Coal Transport strategic corridor

The HaO-Ji Railway is not a passenger line. It is a dedicated heavy-haul coal railway stretching 1,837 kilometers from Inner Mongolia to Jiangxi, designed to move 200 million tons of coal annually from China’s northern producing regions to the energy-hungry central and southern provinces.16

Jingzhou became a node on this corridor.

The bridge connected Jingzhou’s northern industrial zone (Jingzhou Economic and Technological Development Zone) directly to公安 County on the south bank and, more critically, to the national rail network oriented north-south rather than east-west.

Why this mattered for this deep dive: Paper mills require three inputs in massive quantities: water, energy and fiber (virgin pulp or recycled wastepaper). The HaO-Ji Railway gave Jingzhou access to Inner Mongolian coal at transport costs that undercut mills relying on coastal coal deliveries. Simultaneously, the Yangtze gave Jingzhou access to imported wastepaper via Shanghai’s ports, shipped upstream at barge rates.

No other inland paper cluster in China had both: cheap north-south coal rail and cheap east-west river freight.

The Convergence

By 2021, the three conditions had converged; National Economic Zone (2011) + Industrial Transfer Demonstration Zone (2011) + Regional Central City designation (2021) + Yangtze rail cum road bridge + HaO-Ji Railway + Yangtze waterway 2019–2021.17

Jingzhou was no longer a pass through. It was a designated destination.

The only remaining question: what industry would claim the space?

THE FIVE ENGINEERING LEVERS

How Jingzhou is building the paper capital; not describing, but extracting mechanism.

Jingzhou did not wait for paper mills to arrive organically. Between 2017 and 2022, the city deployed five distinct engineering levers; anchor recruitment, policy orchestration, technology leapfrog, vertical integration and category declaration to assemble a greenfield paper cluster at national scale. Each lever is examined in sequence.

Lever 1: Anchor Recruitment

Jingzhou began with a structural insight: legacy paper capitals could not rebuild. Dongguan, Zhenjiang and Shandong’s mill complexes were land constrained, environmentally burdened and equipped with aging machinery that could not be retrofitted without shutting down production. Jingzhou offered the opposite: greenfield sites, abundant water and a provincial government willing to deploy patient capital.

The city recruited four publicly listed paper giants:

Nine Dragons Paper; China’s largest paper producer by volume

Shanying Paper

Xianhe Paper

Longchen (Rongcheng)

Combined committed investment exceeded 55 billion RMB. Total production capacity reached 12 million tons annually for packaging paper and household paper products, with some sources estimating 15 million tons.18

The recruitment was not passive. Jingzhou’s Economic and Technological Development Zone upgraded to national status in 2011, provided the legal infrastructure for large scale industrial land conversion. By the end of 2017, 427 companies above designated size had settled in the zone, including 77 hi-tech enterprises, with industrial output above designated scale reaching 96.19 billion yuan.19 The paper anchors arrived on a platform already built for them.

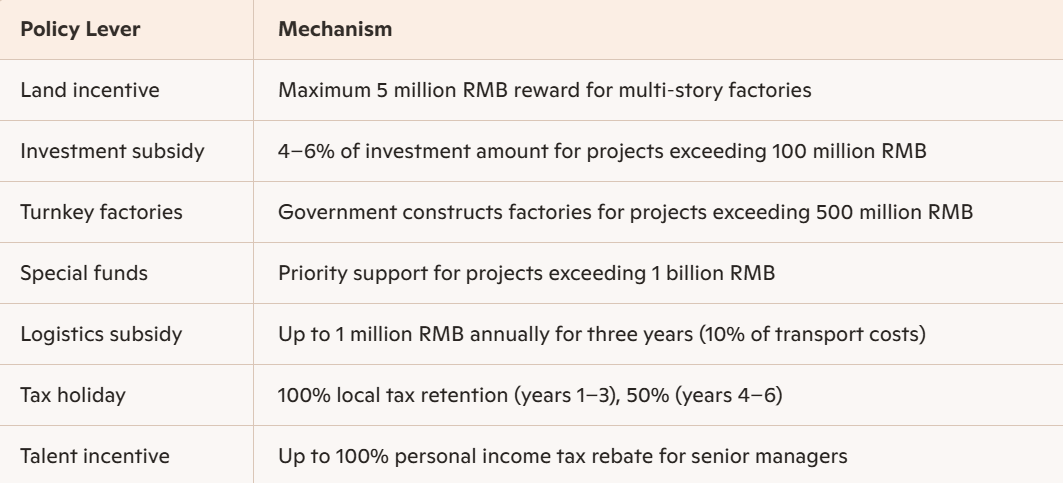

Lever 2: Policy Orchestration

Anchor recruitment required more than land. It required a fiscal engineering stack that lowered risk perception for billion-yuan investments.

The Jingzhou municipal government published a formal incentive structure targeting precisely the paper industry:

This is not generic incentives. This is targeted fiscal engineering; the city treating public funds as patient capital to solve the coordination problem that typically kills greenfield industrial clusters.

The policy stack was enabled by two prior designations. First, the 2011 upgrade to a National Economic and Technological Development Zone gave Jingzhou direct access to central government infrastructure funds, preferential land conversion quotas and elevated investment approval authority.20 Second, the December 2011 designation as a National Industrial Transfer Demonstration Zone explicitly authorized Jingzhou to receive industries relocating from coastal provinces.21

Lever 3: Technology Leapfrog

Legacy paper bases cannot install world leading technology without shutting down production. Jingzhou had no such constraint. Its greenfield mills installed leapfrog equipment from day zero.

The Shanying Case Study

Shanying Paper’s Jingzhou mill, which commenced production in September 2019, was built with Finnish Valmet supplied production lines featuring:

8 meter web width

1,500 meters per minute operating speed

93 bar high pressure steam CFB boilers

100% white water recycling systems

95%+ fiber utilization rates

Automated logistics with predictive maintenance

The mill burns its own waste; sludge, light slag and biogas for power generation, achieving 94%+ production efficiency with self managed control systems. Ultra low emission flue gas meets or exceeds national standards.

The lightweight packaging innovation is particularly notable: Shanying produces 70–130 g/m² linerboard, significantly lighter than traditional grades, reducing raw material consumption while maintaining structural strength. Per ton of product, the PM21 line achieves consumption figures significantly lower than industry standard with white water recycled at nearly 100%, waste slag fully incinerated for power, and treated wastewater meeting discharge standards of 26mg/L COD, below the national standard of 50mg/L.22

Legacy mills cannot retrofit to these specifications. Jingzhou installed them before the first roll came off the line.

Lever 4: Vertical Integration

Jingzhou is not building isolated factories. The city is engineering a closed loop industrial stack:

Input → Pulp → Paper → Power → Packaging

The circular economy loop operates as follows:

Light slag, sludge and biogas from paper production become fuel for CFB boilers

Boilers generate steam and electricity returned to the paper machines

100% of white water is recycled

Solid waste after classification is incinerated for additional power

Treated wastewater meets ultra low discharge standards (COD at 26mg/L vs. national standard of 50mg/L)

Downstream, the cluster has attracted packaging and printing businesses; not accidentally, but through active government recruitment of the full stack. The goal is to capture margin at every stage and reduce external dependencies that could be exploited by competitors.

Lever 5: Category Declaration

The most distinctive engineering move occurred before full build out.

The Jingzhou municipal government formally declared its target on the official investment portal:

“By the end of the 14th Five Year Plan period, Jingzhou will establish itself as Central China’s Packaging Paper Capital, creating a new industrial identity.”23

This is not marketing. It is a policy weapon serving four functions:

Signals certainty to investors still deciding between locations

Pre-empts competitors; Xiaogan dominates household paper; Jingzhou claims packaging

Mobilizes bureaucracy around a measurable, binding target

Creates narrative lock in, backing out becomes politically costly

The declaration was reinforced by the 2021 designation of Jingzhou as a regional central city in Hubei’s 14th Five Year Plan for New Urbanization (2021–2035).24 Hubei Party Secretary Ying Yong, during a 2021 inspection, stated: Jingzhou is the root of Chu culture. Hubei is the center of central China; Jingzhou is the center of Hubei. Central Hubei needs a central city. Jingzhou is duty-bound.25 The category declaration and the regional center designation converged to lock Jingzhou’s paper capital identity into provincial policy.

The Convergence of Levers

Each lever alone would have been insufficient. Anchor recruitment without policy orchestration would have lost bids to competing cities. Policy orchestration without technology leapfrog would have produced a low-margin cluster, not a premium one. Technology leapfrog without vertical integration would have left margin capture incomplete. And none of it would have crystallized without the category declaration that named the target before competitors could react.

The sequence is the strategy. Jingzhou did not wait to win before declaring itself the capital. It declared itself the capital to win.

THE COMPETITIVE MOAT

Why this cannot be copied.

Jingzhou’s engineering blueprint is replicable in theory. In practice, four structural barriers protect the city from competitors who might attempt the same gambit. These barriers are not technological. They are temporal spatial, and political. The moat is not what Jingzhou built. It is what legacy capitals cannot undo and what potential rivals cannot pre-empt.

The Greenfield Advantage That Cannot Be Retrofitted

Legacy paper capitals face a fatal constraint: they cannot rebuild without shutting down.

Shandong produced 20.15 million tons of paper in 2022, ranking first nationally. Guangdong produced 19.69 million tons, ranking second. These are not small industries. They are multi-decade accumulations of capital, labor and infrastructure and multi decade accumulations of technical debt.26

The average paper mill in Guangdong’s Dongguan cluster was built in the 1990s or early 2000s. Its machinery was state of the art at installation. Twenty five years later, that machinery is a liability. Retrofitting a legacy mill to Valmet OptiConcept M specifications; with 1,500 m/min speeds, 100 percent white water recycling and integrated waste to power requires a complete production stoppage of six to eighteen months per line.27 During that stoppage, the mill generates zero revenue while fixed costs continue. Most cannot afford the pause.

Jingzhou had no such constraint. Its mills were built to 2020s specifications from the first foundation pour. The Shanying mill achieved 94 percent production efficiency within months of commissioning. Legacy mills in Guangdong operate at 70–75 percent efficiency due to equipment age and incremental retrofits that never achieved full optimization.28

The math is inexorable: Jingzhou’s mills produce more output per ton of input, per kilowatt hour, per liter of water and they started from zero. Legacy mills cannot close this efficiency gap without a shutdown they cannot survive.

Moat mechanism is basically Temporal lock in. The old capital is trapped in its own capital stock.

The Geographic Convergence That Cannot Be Replicated

Jingzhou occupies a specific position on China’s logistics map that no other inland city can duplicate simultaneously.

The Yangtze Waterway delivers imported wastepaper from Shanghai’s deep-water ports at barge rates that undercut rail transport by approximately 40 percent for bulk commodities. A mill in Shandong or Hebei must pay rail or truck rates for imported fiber. Jingzhou pays barge rates.29

The HaO-Ji Railway delivers Inner Mongolian coal at transport costs that undercut coastal rail deliveries by approximately 30 percent. The 1,837 kilometer heavy haul line was built specifically to move coal from north to south. Jingzhou sits on it. Guangdong does not. Jiangsu does not. Zhejiang does not.30

The combined effect: Jingzhou’s mills access the two most expensive inputs; fiber and energy at a cost structure that legacy coastal mills cannot match. Coastal mills pay less for imported fiber (port adjacency) but more for energy (no cheap coal rail). Northern mills pay less for coal but more for imported fiber (no Yangtze access). Jingzhou pays less for both.31

No other Chinese city currently possesses this dual access. The HaO-Ji Railway is not expanding to the coast. The Yangtze is not rerouting north. The convergence is geologically fixed.

The Moat mechanism is Spatial monopoly. The vector intersection cannot be redrawn.

The Designation Sequence That Cannot Be Pre-empted

Jingzhou declared itself Central China’s Packaging Paper Capital before full build out. This was not boast. It was pre-emption.

Category sovereignty in industrial policy operates on first mover logic. Once a city formally designates itself as the capital of a specific industrial subcategory; packaging paper, not household paper; Central China, not all China; competitors face a coordination problem. A rival city (Yichang, Xiangyang, Yueyang) could declare itself the same title. But doing so would trigger direct competition with an already declared target backed by provincial policy. Municipal bureaucracies avoid this. The cost of a contested title exceeds the benefit.

The 2021 Regional Central City designation reinforced the lock. Jingzhou was one of only six comprehensive regional centers in Hubei.32 Xiaogan; the dominant household paper cluster received no such designation for industrial paper. The provincial government had effectively chosen its champion for each subcategory.

Xiaogan specializes in tissue and household paper (Hengan, Vinda, Zhongshun). Jingzhou specializes in industrial packaging paper, white cardboard and cigarette cardboard. The subcategories do not overlap. A competitor entering Jingzhou’s subcategory would need to recruit the same four anchor firms; Nine Dragons, Shanying, Xianhe, Rongcheng away from a site where they have already sunk billions in committed capital. This is not impossible. It is implausible. The switching costs are prohibitive.33

Political pre-emption is the Moat Mechanism. The title is taken. The anchors are sunk. The category is closed.

The Vertical Integration That Cannot Be Unbundled

Jingzhou’s cluster is not a collection of independent mills. It is a closed loop system where waste from one process becomes fuel for another.

The circular economy architecture:

Paper mill waste (sludge, light slag, biogas) → CFB boiler fuel → steam and electricity returned to paper machines

100 percent white water recycled on site

Solid waste after classification incinerated for additional power

Treated wastewater discharged at 26mg/L COD, below the national standard of 50mg/L

This system has two moat effects. First, it lowers variable costs permanently. A mill that generates its own power from its own waste does not face energy price volatility. A mill that recycles 100 percent of its water does not face water scarcity or rising tariffs. Second, it creates switching costs for any anchor firm considering relocation. A mill built as part of an integrated ecosystem cannot simply pack up and move to a competitor’s site. The ecosystem is not portable.⁹

Legacy capitals cannot easily replicate this integration. Their mills were built incrementally, not master planned. Waste to-power requires adjacent land for boilers and incinerators; land that is already occupied or environmentally restricted. Water recycling requires retrofitting pipe networks that run under active production floors. The cost of integrating a legacy cluster to Jingzhou’s specifications approximates the cost of demolishing and rebuilding it. Which, as established, legacy capitals cannot afford.

Moat mechanism is Architectural lock in. The system cannot be unbundled without destroying it.

The Composite Moat

Each barrier alone is surmountable. A legacy mill could theoretically raise capital for a complete retrofit. A competitor could theoretically build a new rail spur or secure alternative fiber logistics. A rival city could theoretically declare itself a packaging paper capital and compete for anchors. A new entrant could theoretically build a vertical stack from scratch.

The moat is not any single barrier. It is the convergence of all four simultaneously.

To compete with Jingzhou, a rival would need greenfield land with dual logistics access, a pre-emptive policy declaration backed by provincial authority, four anchor firms willing to sink 55 billion RMB and a closed-loop ecosystem engineered from scratch; all while Jingzhou continues to scale its existing cluster. This is not a competitive landscape. It is a moat.

The Greenfield Gambit (Transferable)

What others can extract.

")

This is not a city playbook. It is a leverage point for anyone who has ever looked at an incumbent and realized: they cannot move.

Jingzhou’s engineering reveals a transferable logic that applies to firms, products, careers and projects not just industrial policy. The principle is not about paper. It is about the structural advantage of building from scratch while the established player is frozen by its own success.

The Principle in One Sentence

When incumbents are trapped by their own capital stock, greenfield entrants can win not by competing on quality or price but by installing leapfrog capability, declaring category sovereignty, and forcing the incumbent to defend a position they cannot rebuild.

The Three Conditions for Deploying the Gambit

Before you can execute, you must verify that the incumbent is actually trapped. Three diagnostic questions:

1. Is the incumbent’s core asset also its liability?

Legacy paper mills had world class equipment, in 1995. Twenty years later, that equipment cannot be replaced without shutting down revenue. The mill is trapped. The very capital that made it dominant now prevents it from modernizing.

For you: What does your incumbent own that they cannot afford to replace? A software architecture? A distribution network? A brand positioned so specifically that pivoting would alienate their base? That asset is their cage.

2. Does the incumbent face a coordination problem that you do not?

Jingzhou’s greenfield site required no retrofitting, no union negotiation, no environmental remediation of a century of pollution. The incumbent faced all three. Jingzhou faced none.

For you: What approvals, integrations, or legacy obligations would your incumbent need to manage that you can simply skip? Legacy debt? Legacy partnerships? Legacy pricing commitments? Each skip is a month of speed.

3. Can you declare the category before they react?

Jingzhou declared itself Central China’s Packaging Paper Capital before full build-out. The declaration was not a boast. It was a pre-emption. Once the title was taken, any competitor would have to fight for it and fighting for a declared title is more expensive than claiming an undeclared one.

For you: What category could you name yourself into that your incumbent cannot credibly claim without abandoning their existing positioning? The fastest. The simplest. The first built for [new constraint]. The declaration is a weapon. Use it early.

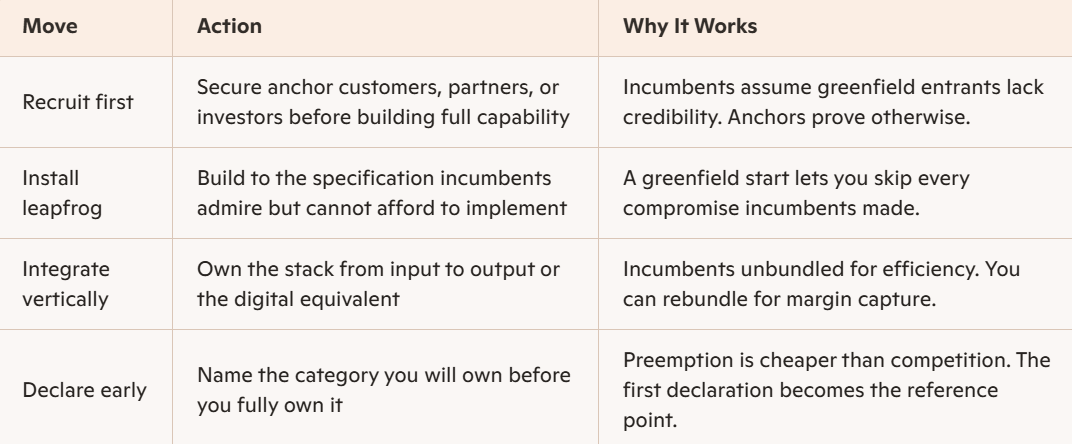

The Four Moves of the Greenfield Gambit

If the three conditions hold, execute in sequence.

The Anti Conditions: When Not to Use This

The Greenfield Gambit fails in three scenarios:

Do not use it if the incumbent can move as fast as you. Some incumbents are not trapped. They are simply large. If your competitor can greenfield alongside you; same technology, same speed, same capital you have no advantage. The gambit only works when incumbents cannot follow.

Do not use it if the category is already contested by multiple declared capitals. If three cities have already declared themselves the X capital, the title has no value. Category sovereignty requires scarcity of declaration. One winner. Maybe two. Not three.

Do not use it if your greenfield advantage is temporary. Jingzhou’s dual logistics access (Yangtze + HaO-Ji) is geographically fixed. A rival cannot build a second Yangtze. If your advantage can be copied in 12 months, you are not building a moat. You are renting a head start.

The Transfer: From City to Individual

You are not a municipal government. You do not control land conversion quotas or provincial policy designations. But you face incumbents; in your industry, your market, your career who are trapped by their own success.

The incumbent firm with a legacy product line that cannot be rewritten without breaking customer integrations. You build the greenfield alternative with no technical debt.

The incumbent professional who has spent twenty years mastering a skillset that is becoming automated. You learn the skill that replaces theirs—and you declare yourself the expert before they retool.

The incumbent platform with a network effect so dense that any change alienates their base. You build the adjacent space they cannot enter without cannibalizing themselves.

In each case, the logic holds: incumbents are frozen. You are not. Build leapfrog. Declare early. Do not ask for permission. The only question is whether you recognize the trap they are standing in before they do.

The Test

Before you deploy the gambit, ask one question:

If my incumbent wanted to do what I am about to do, how long would it take them and what would they have to break to get there?

If the answer is longer than 18 months and includes at least one thing they cannot afford to break, the gambit is viable. Build. Declare. Move.

Jingzhou did not wait for permission to become the Paper Capital. It built the cluster, declared the title, and let the legacy capitals watch from their frozen ground.

You can do the same. You just have to find the thing they cannot afford to replace.

THE RISK & UNCERTAINTY

What could break the model.

The Greenfield Gambit is not a guaranteed victory. It is a calculated bet against frozen incumbents. Jingzhou’s engineering blueprint has delivered 12–15 million tons of capacity and four anchor firms. But five structural risks could break the model and each risk carries a lesson for anyone attempting the same gambit in their own domain.

Risk 1: Winning a Race You Cannot Stop

National Overcapacity

The global paper industry is already oversupplied. Current worldwide capacity utilization sits at approximately 75 percent, meaning one quarter of existing production capacity is idle. This oversupply resulted from a simple arithmetic failure: the rate of new production lines coming online exceeded the rate of market demand growth.34

Jingzhou added 12–15 million tons of new capacity in a single planning cycle. That is not incremental growth. It is a supply shock.

The risk is not that Jingzhou’s mills are inefficient. They are hyper efficient. The risk is that efficiency does not matter when the entire industry is producing more than the market will buy. In an oversupplied market, the marginal producer no matter how efficient faces margin compression. And if the oversupply is structural rather than cyclical, the compression is permanent.

The Greenfield Gambit assumes that leapfrog efficiency creates a permanent moat. But if the entire industry is overcapacity, efficiency only determines who bleeds slowest. The real risk is winning a race you cannot stop; building capacity faster than demand grows, then discovering that demand has a ceiling you did not model.

Jingzhou’s anchors have diversified into specialty grades (cigarette cardboard, white cardboard, lightweight linerboard) that face less price pressure than commodity packaging paper.35 The lesson: greenfield efficiency is not enough. You must also enter a subcategory where overcapacity is less severe or accept that you are betting on demand growth that may not arrive.

Risk 2: The Policy That Giveth Can Taketh Away

Environmental Re-Regulation

Jingzhou’s gambit relied on a specific policy window: paper was removed from the two high (high pollution, high energy) list, enabling rapid permitting and financing.36 That window could close.

The Yangtze River Protection Law, effective March 1, 2021, established the most stringent water protection regime in China’s history.37 The Jingzhou section of the Yangtze, 483 kilometers long, accounting for nearly half of the river’s length within Hubei falls directly under this jurisdiction.

The law mandates:

A ten year fishing ban in key areas of the Yangtze Basin, effective January 1, 202038

Strict controls on sewage outlets, with Jingzhou required to upgrade 1,824 outlets under a one policy for one outlet framework39

Phased implementation of wastewater discharge permits in four industries, including papermaking, by the end of 2023

Jingzhou’s mills currently meet or exceed these standards. The Shanying mill discharges treated wastewater at 26mg/L COD, below the national standard of 50mg/L.40 But standards can tighten faster than mills can adapt. If the Yangtze River Protection Law is amended to impose stricter limits on industrial water consumption or wastewater chemistry, even compliant mills face retrofitting costs—and retrofitting a greenfield mill, while cheaper than retrofitting a legacy one, is not free.

The deeper risk is political. Jingzhou’s Regional Central City designation was granted by the Hubei provincial government. But environmental regulation is enforced by the Ministry of Ecology and Environment, which operates on a different mandate. A conflict between provincial industrial policy and national environmental policy would not necessarily resolve in Jingzhou’s favor.

Policy giveth, and policy taketh away. The same government that designated you a regional center can reclassify your industry as high pollution tomorrow. Your gambit is only as secure as the policy coalition that enabled it and that coalition can shift.

Jingzhou has pre-emptively integrated environmental compliance into its engineering. The circular economy loop (waste to power, 100% water recycling) is not just efficiency. It is political insurance. A mill that discharges at 26mg/L COD is harder to shut down than a mill that barely meets the standard. The lesson: build to a standard stricter than regulation requires. The extra cost is insurance against regulatory capture.

Risk 3: Four Firms, One Cluster

Anchor Concentration

Jingzhou’s paper capacity is concentrated in four publicly listed firms: Nine Dragons, Shanying, Xianhe, and Rongcheng.41 This is a feature of the gambit anchor recruitment creates critical mass but it is also a vulnerability.

If one anchor firm faces financial distress, the entire cluster feels it. If two anchors reduce capacity simultaneously, the cluster’s logistics infrastructure (designed for 12–15 million tons) becomes underutilized, raising per unit costs for remaining firms. And if an anchor relocates, unlikely given sunk capital, but not impossible the loss is not just capacity but signaling. Other firms interpret a departure as a negative signal about the location.

The 2025 anti-inflation initiative in the paper industry suggests margin pressure is real. The Guangdong provincial paper association issued the industry’s first anti-inflation 倡议书 in July 2025, explicitly calling for an end to low price disorderly competition and dumping below cost.42 That is not a statement of health. It is a statement of distress.

Anchor concentration is a double edged sword. Fewer anchors mean easier coordination but also higher single point of failure risk. The gambit assumes anchors are committed because their capital is sunk. But capital can be written off. The real commitment is not the factory. It is the expectation of future profit. When that expectation collapses, anchors do not stay because they cannot leave. They leave because they must.

Jingzhou’s vertical integration (paper → packaging → printing) creates switching costs for anchors.43 A mill that supplies downstream packaging plants within the same zone cannot easily relocate without breaking those customer relationships. The lesson: lock anchors not just with sunk capital, but with ecosystem dependency. Make leaving more expensive than staying; not because of the factory, but because of the customers they would abandon.

Risk 4: The Geography That Giveth Can Be Rerouted

Logistics Bypass

Jingzhou’s dual logistics access Yangtze barges for imported wastepaper, HaO-Ji Railway for Inner Mongolian coal is a structural moat. But moats can be bridged.

If a competing inland city develops alternative logistics a new rail spur, a different port connection, a subsidy that undercuts barge rates; Jingzhou’s cost advantage erodes. The risk is not that the Yangtze moves. The risk is that the economics of paper production shift. If imported wastepaper becomes less critical (due to domestic recycling improvements) or if coal becomes less critical (due to energy transition), the vectors that made Jingzhou uniquely positioned become less valuable.

The HaO-Ji Railway was built as a coal corridor. China’s energy transition toward renewables, away from coal could reduce coal volumes on the line over time. Lower coal volumes mean higher per unit transport costs for remaining coal shippers, eroding Jingzhou’s cost advantage. The mill that was built to burn Inner Mongolian coal may find itself paying more for that coal than it modeled.

Geographic moats are durable, but not permanent. They depend on the continued relevance of the flows they capture. When the flows change; because of technology, policy, or markets the moat becomes a relic. The gambler who built on a specific vector must monitor not just the competitor, but the vector itself.

Jingzhou’s paper mills are not coal-dependent in the same way as northern mills. They use coal for power generation, but the waste to power loop reduces external coal consumption. The lesson: do not build on a single vector. Build redundancy into your input economics. If coal prices rise, your ability to generate power from waste becomes not just efficiency, but survival.

Risk 5: Declared Capital Without Delivered Scale

The Hollow Title

Jingzhou declared itself Central China’s Packaging Paper Capital before full build out. That declaration was a pre-emptive weapon. But a title without delivered scale is hollow.

If capacity targets are missed; if the 15 million tons becomes 10 million tons, if downstream integration stalls, if anchor firms delay expansion the declaration becomes a liability. Competitors can point to the gap between declaration and delivery. Investors can question credibility. And the provincial government that designated Jingzhou as a regional center can quietly redirect infrastructure investment elsewhere.

The declaration is a commitment device. It forces the city to deliver. But commitment devices only work if delivery is actually possible. If structural constraints (environmental, financial, logistical) prevent full build out, the declaration becomes a trap rather than a weapon.

Declaring early is powerful. Declaring without the capacity to deliver is self destruction. The gambit requires not just the confidence to name the category, but the ruthless realism to know whether you can actually own it. A hollow declaration is worse than no declaration. It signals overreach.

Jingzhou declared only after anchors were recruited and capacity was under construction. The title was not aspirational in the sense of we hope to get there. It was declarative in the sense of we are already building this. The lesson: declare early, but only after the first concrete has been poured. Aspirational titles are cheap. Titles backed by sunk capital are credible.

The Single Point of Failure

Across all five risks, one vulnerability recurs: Jingzhou’s gambit depends on continuous demand growth.

Overcapacity is only a problem if demand does not grow into the supply. Environmental regulation is only a constraint if demand cannot absorb compliance costs. Anchor concentration is only fatal if declining margins drive exits. Logistics bypass is only threatening if demand shifts to alternative supply chains. The hollow title is only exposed if demand fails to materialize and capacity sits idle.

The unspoken assumption beneath the Greenfield Gambit is that the market will grow to meet the capacity you built. If that assumption fails, every other mitigation collapses.

Jingzhou is betting that central China’s packaging paper demand; driven by e-commerce, manufacturing, and consumer goods will continue its historical growth trajectory. That is a reasonable bet. But it is still a bet.

And the house does not always win.

For the Reader: Your Risk Audit

If you are deploying the Greenfield Gambit in your own domain, audit your risks with the same forensic clarity:

Overcapacity risk: Is your industry already oversupplied? If yes, efficiency alone will not save you. You need a subcategory with tighter supply.

Policy re-regulation risk: Does your advantage depend on a specific regulatory window? If that window closes, can you survive?

Concentration risk: Are you dependent on a small number of anchors? If one leaves, does the system break?

Vector risk: Does your moat depend on a specific flow (logistics, data, attention) that could be rerouted? If that flow changes, are you still advantaged?

Credibility risk: Did you declare before you could deliver? If delivery stalls, can you recover credibility or did you mortgage it for a title you cannot redeem?

The Greenfield Gambit is not a formula. It is a diagnosis. You are betting that incumbents cannot move, that greenfield speed beats legacy depth, that declaring early pre-empts competition, and that demand will grow into the capacity you built.

Those are four bets. Any one of them can lose.

Jingzhou’s engineering is impressive. But impressive engineering does not repeal the laws of markets, politics, or physics. It only postpones their judgment.

CONCLUSION

Jingzhou’s gambit reveals something uncomfortable about economic development.

The standard playbook assumes that heritage matters. That centuries of craft knowledge, generational firms, and accumulated capital create an unassailable advantage. That poor places become rich by climbing a ladder of incremental upgrades; better roads, better schools, better certification, better branding.

Jingzhou did not climb that ladder. It built a new ladder from scratch while the old capitals stood on theirs, unable to move.

The implication is not that heritage has no value. It is that heritage can become a liability faster than anyone expects. The same capital stock that made Guangdong and Shandong dominant in paper now prevents them from rebuilding. They won the last era. They are losing this one. Not because Jingzhou out competed them. Because they cannot compete at all. They are frozen.

This is the deeper pattern.

Every industry, every market, every profession eventually produces incumbents who are trapped by their own success. Their assets become constraints. Their advantages become anchors. They cannot rewrite the code base. They cannot retool the factory. They cannot abandon the brand position that made them rich but now makes them irrelevant.

And somewhere, a greenfield entrant is watching. Building from zero. Installing leapfrog capability. Declaring a new category before the incumbent can react.

Jingzhou is not a story about paper. It is a story about the moment when the frozen incumbent looks up and realizes the race has already left them.

The only question is whether you are the incumbent or the entrant.

Next Week: Zhangjiajie

Jingzhou proved that a replaceable pass through can become irreplaceable by building from scratch while incumbents stand frozen. The Greenfield Gambit is not about paper. It is about recognizing when the old capital cannot follow.

But what if there is no incumbent to disrupt? What if the asset is not an industry to build, but a landscape that already exists?

The city we cover next week, Zhangjiajie; faced the opposite problem. The asset was already there, a cluster of quartz sandstone pillars that needed no improvement. The problem was capture. The mountain drew the crowd. The city kept none of the value.

Jingzhou solved for creation.

Zhangjiajie solved for capture.

Two different problems. Two different principles.

Next week, we audit how.

Hubei Provincial Bureau of Statistics, Hubei Statistical Yearbook 1996 (Beijing: China Statistics Press, 1996), table 2-18 Gross Domestic Product by Prefecture, City, and County.

Hubei Provincial Bureau of Statistics, Hubei Statistical Yearbook 1996, table 2-1: Gross Domestic Product of Hubei Province (1978-1995)

Hubei Provincial Bureau of Statistics, Hubei Statistical Yearbook 1996, table 2-18.

National Bureau of Statistics, China Statistical Yearbook 1996 (Beijing: China Statistics Press, 1996), table 3-1: Gross Domestic Product and Per Capita GDP.

Hubei Provincial Government, "From 72% to 106%: How Hubei Caught Up to the National Average," Hubei Daily, October 31, 2016.

Jingzhou government investment portal

Hubei Provincial People’s Government, “Jingzhou Economic & Technological Development Zone,” en.hubei.gov.cn, October 13, 2015.

China Daily, “Jingzhou Economic and Technology Development Zone,” govt.chinadaily.com.cn, January 13, 2019.

Jingzhou Municipal Government, “Jingzhou Economic & Technological Development Zone,” Jingzhou Investment Portal, updated June 16, 2021.

Hubei Provincial People’s Government, “Waist-Building Project of Jingzhou Implemented,” en.hubei.gov.cn, May 1, 2012.

e-line Minsheng, “Inquiry on Jingzhou Regional Central City Designation and Official Name,” 2021.

Hubei Provincial Development and Reform Commission, Response to Inquiry on Jingzhou Regional Central City Designation, e-line Minsheng, 2021.

ibid11

Jingzhou Municipal Government, “Jingzhou to be Elevated to Type II Large City,” jingzhou.gov.cn, November 27, 2021.

Baidu Baike, "Jingzhou Yangtze River Rail-cum-Road Bridge," last modified February 5, 2026.

Baidu Baike, "Jingzhou Yangtze River Rail-cum-Road Bridge," last modified February 5, 2026.

Hubei Provincial People’s Government, “Jingzhou Economic & Technological Development Zone,” en.hubei.gov.cn, October 13, 2015.

Jingzhou Municipal Government, “Jingzhou Economic & Technological Development Zone,” Jingzhou Investment Portal, updated June 16, 2021.

Jingzhou Municipal Government, "Jingzhou Economic & Technological Development Zone," Jingzhou Investment Portal, updated June 16, 2021.

China Daily, "Jingzhou Economic and Technology Development Zone," govt.chinadaily.com.cn, January 13, 2019.

Hubei Provincial People's Government, "Jingzhou Economic & Technological Development Zone," en.hubei.gov.cn, October 13, 2015.

Jingzhou News Network, "【新春走基层】人歇机不歇 430名山鹰人奋战忙订单," news.jznews.com.cn, February 16, 2026.

Jingzhou Municipal Government, “Jingzhou Economic & Technological Development Zone,” Jingzhou Investment Portal, updated June 16, 2021.

Hubei Provincial Development and Reform Commission, Response to Inquiry on Jingzhou Regional Central City Designation, e-line Minsheng, 2021.

People's Daily Online Finance, "生態智慧工廠!華中最大工業用紙生產基地正式投產," ccnews.people.com.cn, December 6, 2019.

广东省造纸行业协会, “东莞造纸:从传统制造向绿色智造进发,共筑’纸’上未来!,” gdpaper.cn, April 23, 2025.

纸业网, "造纸行业区域发展格局分析 广东、山东两省造纸优势显著," paper.com.cn, July 3, 2023.

Jingzhou Municipal Government, “Jingzhou Economic & Technological Development Zone,” Jingzhou Investment Portal, June 16, 2021.

Baidu Baike, "Jingzhou Yangtze River Rail-cum-Road Bridge," last modified February 5, 2026.

Valmet, “Shanying Huazhong Paper Industry: Smart and Ecological,” valmet.com, 2021.

Hubei Provincial Development and Reform Commission, Response to Inquiry on Jingzhou Regional Central City Designation, e-line Minsheng, 2021.

Jingzhou Municipal Government, "Jingzhou Economic & Technological Development Zone," op. cit.

人人文库, "2025造纸行业空白市场分析及产能过剩化解投资布局设计解析报告," renrendoc.com, December 27, 2025.

Jingzhou Municipal Government, “Jingzhou Economic & Technological Development Zone,” Jingzhou Investment Portal, June 16, 2021.

Jingzhou News Network, “【新春走基层】人歇机不歇 430名山鹰人奋战忙订单,” news.jznews.com.cn, February 16, 2026.

Zhu Hang, “A River Running Eastward: Pure and Abundant,” cppsup.net.cn, October 30, 2023.

ibid37

Jingzhou Municipal Government, “Jingzhou Lays Down Objectives and Tasks for Ecological Conservation in 2023,” e.jingzhou.gov.cn, April 7, 2023.

ibid36

ibid35

中宏网, “造纸行业首封’反内卷’倡议书发布 行业供给端有望迎来新 轮出清,” gp.zhonghongwang.com, July 29, 2025.

ibid35

Mo, The idea that an incumbent's greatest asset can eventually become its greatest constraint was especially thought-provoking. Jingzhou's story feels less like an industrial analysis and more like a lesson in adaptation, positioning, and recognizing opportunities that others cannot pursue because they're too invested in the past.

Excellent read. Thanks for sharing, Monica